Financial-services loyalty programs often look strong in strategy decks and weak in operations. The concept is easy enough: reward the right customer at the right moment to increase usage, retention, and lifetime value. The hard part is making that happen across products, regions, compliance rules, internal teams, and fulfillment partners without creating even more operational risk.

That gap is getting more expensive. Capgemini's World Retail Banking Report 2025 found that only 26% of cardholders are satisfied with their card experience, while 74% are indifferent or dissatisfied enough to be considered flight risks. The same research found that 47% of prospective customers abandon card onboarding because of a poor experience. McKinsey's 2024 retail banking report argues that banks need deeper primary relationships built through mobile-first journeys, relationship-based incentives, and hyper-personalization. PwC's 2025 customer experience survey adds another warning sign: 52% of consumers say they stopped buying from or using a brand after a bad experience, and 46% of executives believe their current loyalty program will be irrelevant within three years.

For banks, fintechs, and trading platforms, the answer is not "more rewards." It is better loyalty operations.

What loyalty program automation really means

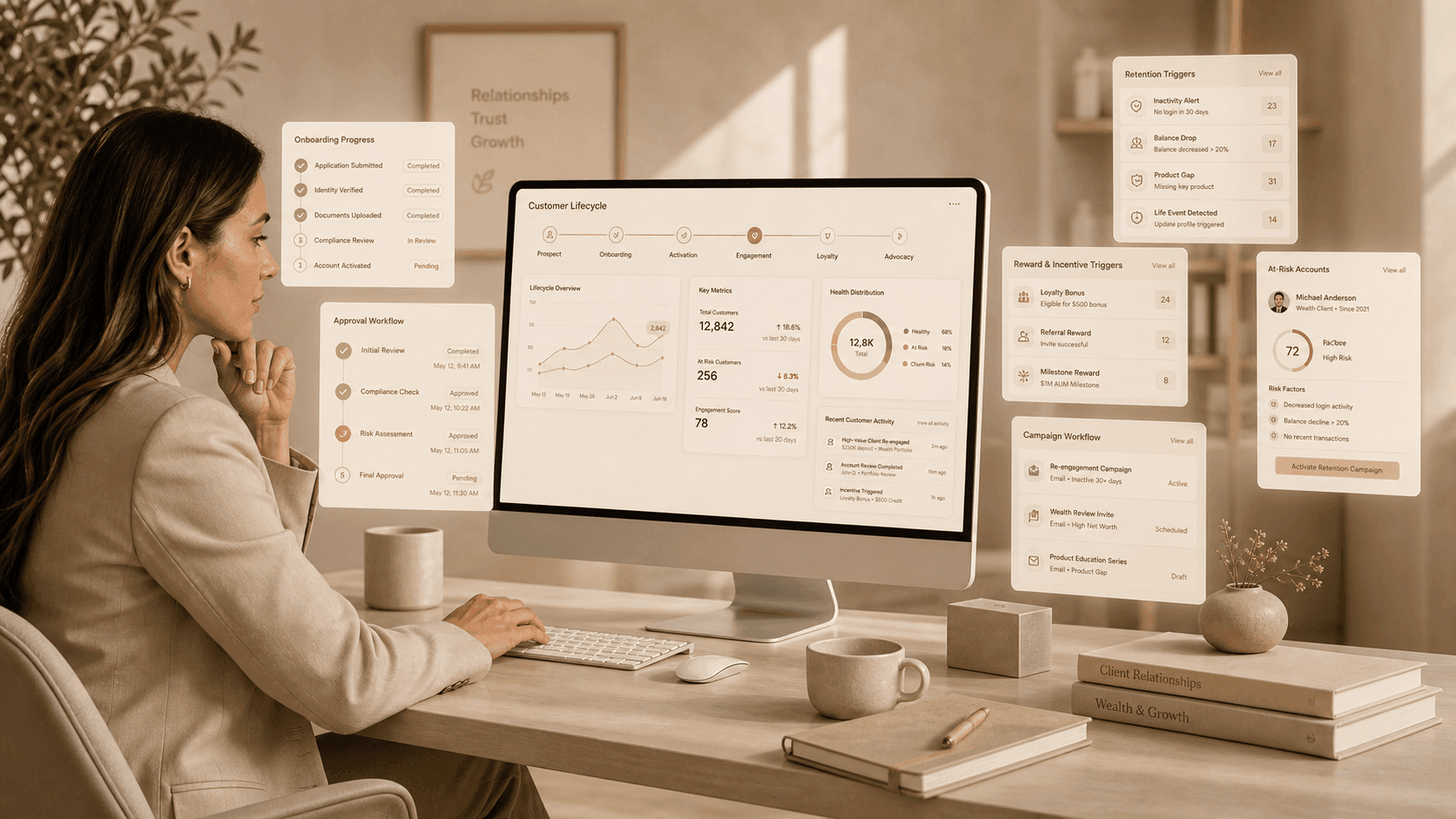

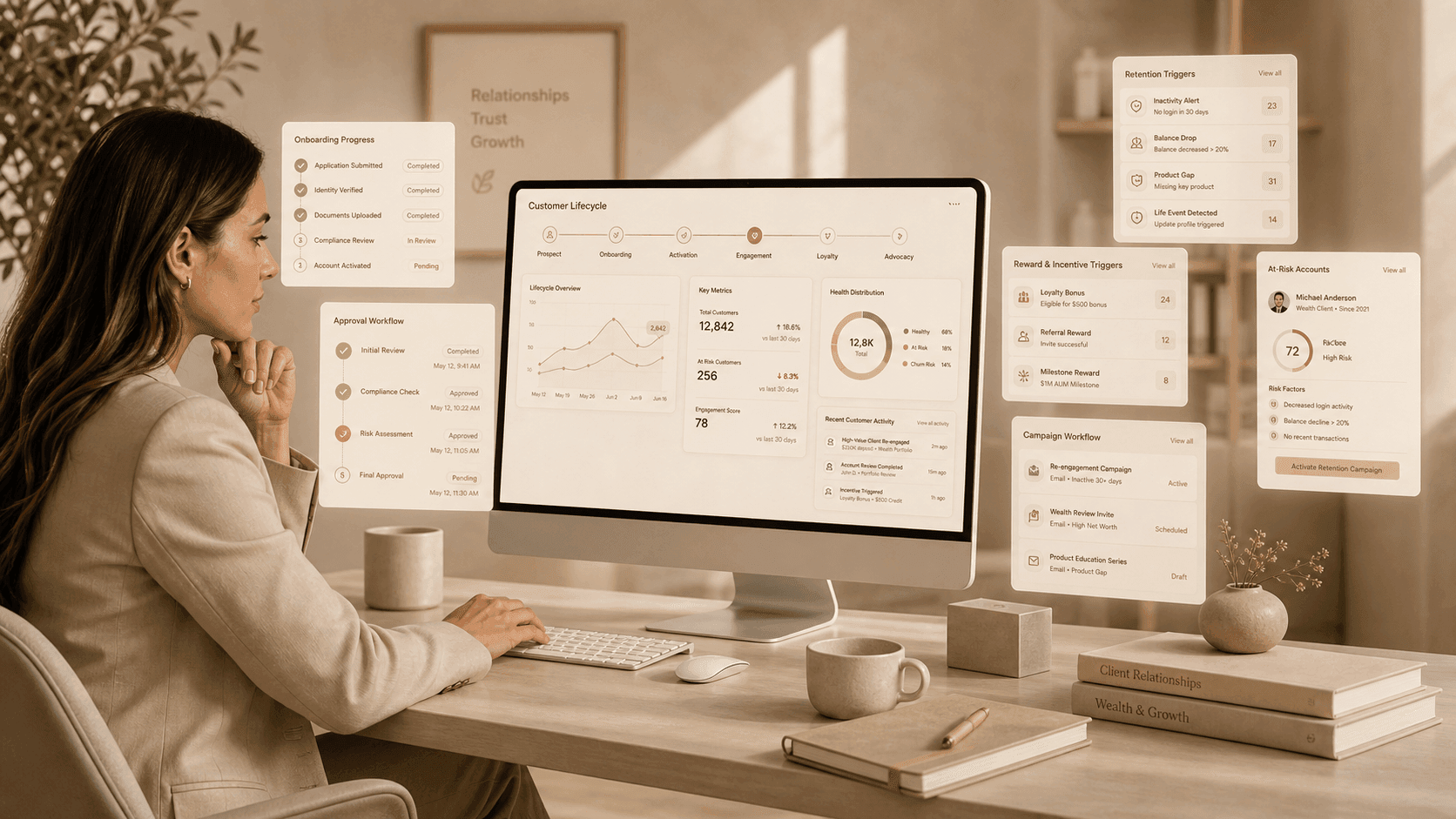

Loyalty program automation is not just sending points after a transaction. In enterprise financial services, it means building a system that can:

- detect meaningful customer events

- decide which incentive fits the customer, segment, and policy rules

- route approvals when needed

- deliver the reward in the right market and channel

- track whether the incentive improved activation, retention, or spend

In other words, automation turns loyalty from a manual marketing campaign into repeatable infrastructure.

That distinction matters because financial-services teams rarely run a single simple program. A bank may have separate rewards logic for cards, deposits, referrals, branch campaigns, and wealth tiers. A fintech may need different flows for KYC completion, first deposit, product adoption, and reactivation. A trading platform may want to reward funded accounts, first trades, education milestones, or VIP retention, but still maintain guardrails around value thresholds, jurisdictional limits, and auditability.

Without a system, all of that work gets stitched together with spreadsheets, emails, local vendors, and manual exceptions.

Why loyalty programs break down in financial services

Most institutions do not fail because they lack ideas. They fail because their operating model cannot support the ideas consistently.

Common breakdown points include:

1. Customer triggers live in too many systems

The moments that should trigger loyalty actions are spread across core systems, apps, CRMs, data warehouses, support platforms, and compliance workflows. If no one can reliably connect those events, the program becomes reactive instead of timely.

2. Approval and policy rules are handled manually

Financial-services teams often need controls around reward value, recipient type, geography, and business purpose. When every exception requires back-and-forth email approvals, speed disappears and teams start avoiding the program altogether.

3. Rewards are generic because personalization does not scale

Capgemini reported in 2025 that 73% of customers feel rewards programs are not personalized enough. That is not surprising. Many teams still rely on a small set of static offers because tailoring rewards across segments, channels, and markets is operationally heavy.

4. Global execution is inconsistent

Digital rewards may work in one market, physical gifts in another, and certain vendors in only a handful of countries. If fulfillment capabilities differ widely by region, customer experience becomes uneven and hard to govern.

5. Measurement stops at redemption

A redeemed reward is not the goal. The goal is better business outcomes: higher activation, deeper product usage, lower churn, more referrals, stronger wallet share, or higher lifetime value. Programs that only measure send volume or redemption rates do not give leadership enough confidence to scale.

A practical framework for loyalty program automation

The strongest programs usually follow the same sequence.

1. Start with behaviors, not perks

PwC's 2025 survey warns that many loyalty programs are designed around the wrong signals. Define what loyalty actually looks like in your business before deciding on the reward.

Useful examples include:

- completing onboarding and funding within a target window

- adopting a second product

- increasing transaction frequency

- returning after a dormant period

- maintaining a high-value relationship without attrition

- referring another qualified user or account

This keeps the program tied to business outcomes instead of generic "engagement."

2. Connect triggers to live business events

The next step is to identify the moments worth automating. In financial services, these often include:

- KYC or KYB approval

- first deposit or first card spend

- first trade or first funded account

- milestone balances or tier changes

- customer anniversaries

- service-recovery moments after complaints or delays

- referrals, renewals, or expansion events

McKinsey notes that mobile has become the primary orchestrator of customer interaction in banking. Loyalty automation should reflect that reality by linking digital product events and CRM data to reward workflows instead of relying on batch exports and delayed campaign logic.

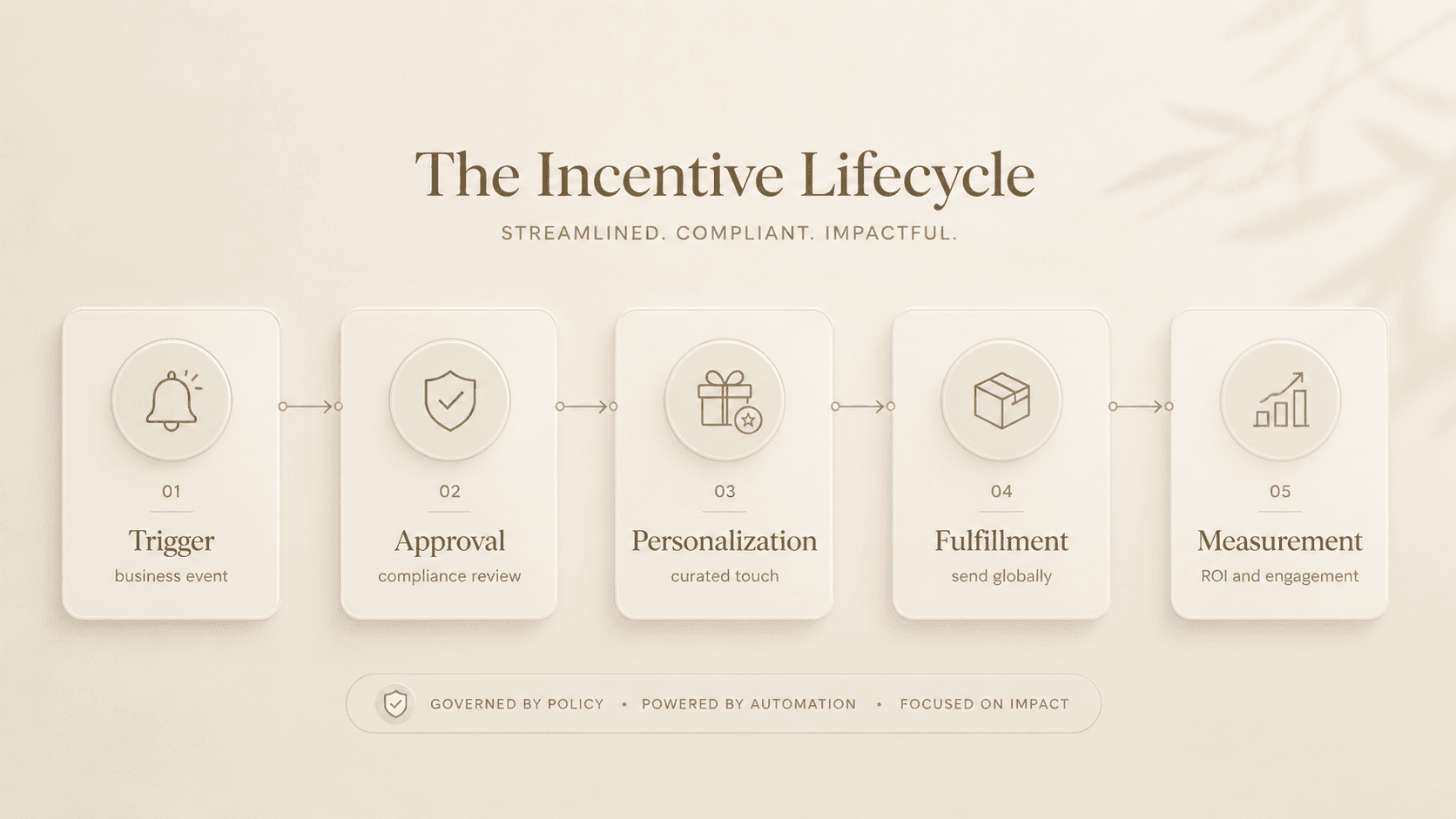

3. Build governance into the workflow

Automation only works in regulated environments if governance is part of the design. That means setting rules for:

- who can trigger a reward

- which events qualify

- maximum reward values by segment or region

- approval routing for higher-risk cases

- required audit fields and reporting

- acceptable reward types by market

This is where many financial-services teams get stuck. They treat compliance review as a separate manual process rather than an embedded workflow layer.

4. Personalize within guardrails

Personalization is not the same as improvisation. Customers want relevance, but financial institutions need consistency and control.

Capgemini found that 86% of customers are willing to share personal information in exchange for better recommendations and rewards, yet only about half receive personalized alerts or advice on how to maximize their rewards. PwC also found that 53% of consumers think sharing personal information is worth it if it makes the experience smoother, but 93% will lose trust if data is mishandled.

The practical lesson is simple: personalize with transparent, defensible inputs. Use known preferences, product behavior, customer tier, geography, and campaign context. Avoid opaque decisioning that teams cannot explain internally.

The best programs usually mix several reward types rather than forcing every customer into the same format:

- points or cashback for frequent transactional behavior

- curated physical gifts for milestone relationships

- branded swag or event kits for community-building moments

- recipient-choice rewards when preferences vary widely

- VIP or experience-based rewards for premium segments

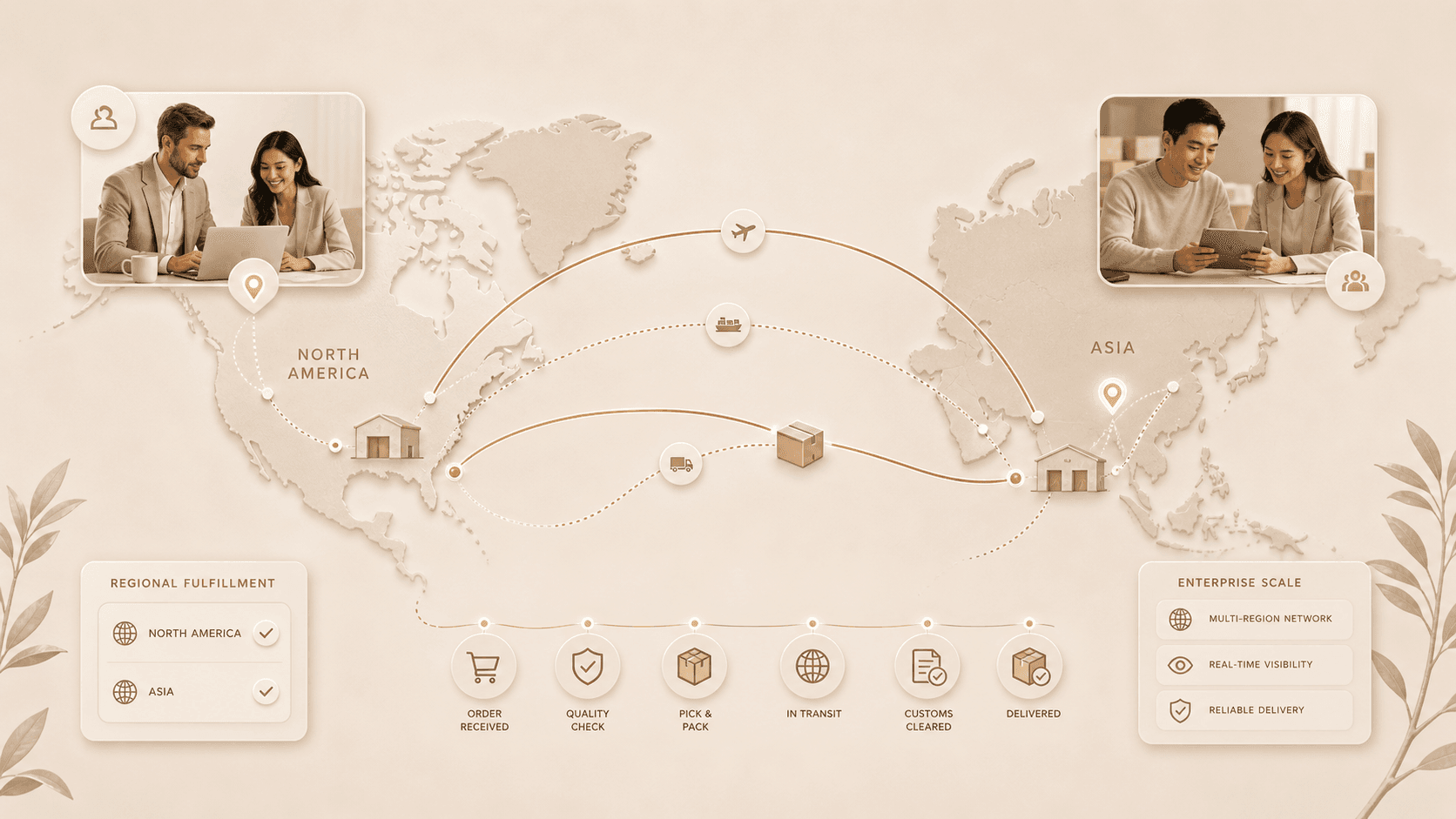

5. Make global fulfillment part of the design

Global loyalty programs fail when delivery is treated as an afterthought. A reward that is easy to send in New York may be hard to source, customize, or deliver in Taipei, Seoul, or Tokyo. That creates service inconsistency precisely where loyalty programs are supposed to build trust.

This is why enterprise teams increasingly need an operating model that combines automation with international execution. A loyalty system should be able to support local relevance, cross-border delivery, customization, and reporting without forcing teams to build different manual processes for every region.

6. Measure outcomes, not activity

The final step is to connect incentives to business metrics leadership actually cares about:

- onboarding completion rate

- time to first transaction

- repeat usage or frequency

- product cross-sell

- churn reduction

- referral rate

- customer lifetime value

- cost per retained customer

This is also where internal buy-in improves. If a loyalty program can show measurable movement in retention or spend, it becomes easier to defend budget, improve policy design, and scale across more business lines.

Giftpack's own Sales ROI Calculator and Customer Success ROI Calculator are useful reminders that relationship programs work better when they are treated as measurable systems rather than soft-touch gestures.

Where to start if your program is still manual

Most teams do not need to automate everything at once. A better starting point is one high-value use case with clear business ownership.

Strong first candidates include:

- card onboarding rewards for approved and funded customers

- first-trade or first-deposit journeys for trading platforms

- reactivation campaigns for dormant but valuable users

- VIP retention moments for wealth or brokerage clients

- customer service recovery for high-value accounts

From there, build the workflow around one trigger set, one approval model, one reward logic, and one measurement dashboard. Once that operating pattern works, it can expand into broader lifecycle journeys.

Why this matters for Giftpack's audience

Giftpack is most compelling when incentive programs stop being a gifting problem and become an infrastructure problem. Enterprise teams in banking, fintech, and trading do not just need a catalog. They need a way to decide, execute, and measure incentives globally across many systems, teams, and markets.

That is where AI incentive decisioning, workflow automation, global fulfillment infrastructure, and measurable reporting start to matter together. The value is not only better rewards. It is less operational drag, stronger governance, more consistent execution, and a clearer line between loyalty spend and business outcomes.

Conclusion

Banks, fintechs, and trading platforms do not need more disconnected loyalty campaigns. They need loyalty operations that can keep up with customer expectations, policy requirements, and international scale.

The teams that win will be the ones that connect real customer triggers to controlled, personalized, and measurable reward workflows. In a market where loyalty is increasingly fragile, automation is no longer a nice-to-have layer on top of the program. It is what makes the program operationally viable.

Read More Recommendations

What Is The Customer Loyalty Ladder? Strategies To Boost Loyalty Levels Link in the early framework section when explaining how loyalty should be tied to observable behaviors and lifecycle stages.

30 Customer Appreciation Day Ideas For Banks To Show Gratitude Link in the examples or activation section when showing campaign moments that can sit inside a broader automated loyalty program.

Sales ROI Calculator: Quantifying Deal Acceleration & Client Relationship Value Through AI-Powered Gifting Link in the measurement section when discussing how to connect relationship programs to business outcomes.

The Guide To Gifting For Clients Link where the article distinguishes between generic gifting and structured loyalty operations.